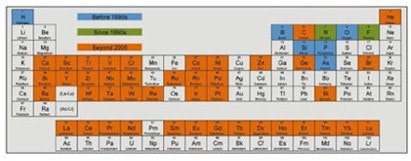

Before the 1990s, silicon chip technology employed only six elements according to IBM. Two more were then added to the chemist's palette but, after 2005, improvements became progressively tougher to achieve, so 42 other elements were employed and today we see a huge variety of compounds, alloys, solvents and dopants brought to bear. This is shown below.

Elements employed in the silicon chip business where blue refers to before the 1990s, green for since the 1990s and red for beyond 2005.

Source: IBM

The much wider choice of chemistry attracted other fine chemical companies to enter the field. For example, SAFC in the $2 billion Sigma-Aldrich™ Group (NASDAQ: SIAL) is one of the world's 10 largest fine chemicals businesses. It created a subsidiary SAFC Hitech™ and bought Intel Capital's investment Epichem in the UK for $60 million to get into mainstream chemicals for the silicon chip industry. It majors on Metalorganic Chemical Vapor Deposition (MOCVD) and Atomic Layer Deposition (ALD) processes on silicon semiconductor substrates. That involves materials for high-k dielectrics in logic and memory devices, additional functional memory architectures, electrodes in DRAM or gate stacks, barrier layers, wiring, and low-k dielectrics eg for crossovers.

In April 2008, it opened a $6 million clean room in the USA to assist in its supply of materials to the silicon and compound semiconductor industries, such as those making conventional GaAs devices.

Today that includes high permittivity transistor dielectrics involving oxides and binary oxides such as aluminum oxides, hafnium oxides, hafnium silicates and zirconium oxides and complex rare earth oxides in its production processes. Recently, hafnium zirconium based layers were targeted as well. They offer greater flexibility because they can be doped with other materials like silicon, nitrogen, aluminum, lanthanum and yttrium to meet individual customer requirements in creating a layer that functions well for a particular device design. Beyond that, the research and development of, for example, lanthanide and strontium chemistries, binary metals and complex metal oxides or iterations of oxides is in the frame.

SAFC Hitech™ has now reached $500 million gorging on the boom in silicon chips and conventional compound devices. However, others such as Toppan Printing have been using a similar choice of elements and compounds to create high permittivity dielectrics and semiconductors in printed transistors and the key elements of many types of printed and partly printed display, sensor, laser and photovoltaics to take just a few examples.

Fine chemical suppliers supporting this next wave include Cabot, Kodak, DuPont and Henkel. Should they wish, fine chemical companies such as SAFC Hitech can also add this more future proof activity or they may be like the wealthy leaders in bottle valves who left it too late to enter the field of transistors. In about five years, such decisions will become critical for those making fine chemicals and associated processes for the electronics industry, not because sales of silicon chips and conventional compound devices will necessarily start to drop but because profits of those involved may be headed south as this conventional business becomes more commoditised and continues its move to East Asia.

To do a comparison with IBM's figures, we cannot ask what materials are marketed in printed transistors because none have been sold. So what has been the evolution of elements employed in printed electronics in general? Before the 1990s we had Cu, Zn and S in screen printed ac electroluminescent displays, Al, Ti and O for insulators and protective layers, Ag for conductors, Ni and C for resistors and In and Sn for transparent electrodes, for example.

Since the 1990s we have added H for polyanilene antistatic coatings and RF shielding and polythiophene conductors, to take a few. Since 2005 we have added Ru, Ga and Se in printed photovoltaics and N in dielectrics and Ca, B, Mn etc in truly printed OLEDs for example. However, in the laboratory are a vast array of printed electronic processes and materials including, just for transistors, printed elements, alloys and compounds involving Si, In, Ga, Se, Ti, Ru, H, O, N, Cd, Se, Pb, La, Zr, Hf , Ba, Ga, As, many of the seventeen rare earth metals in new printed displays and so on, only a few of which have been used before in other printed materials.

Accordingly, from the point of view of the supplier of fine chemicals into the electronics industry, printed electronics is starting to use in volume the breadth of elements and formulations that are appearing in the silicon chip and conventional display industry. There should be nothing surprising in this because the physics and physical chemistry dictate certain structures and formulations for certain electrical properties. However, the chemicals and inks required are very different in most other respects such as morphology and rheology and composites, nano technology and organic compounds are much more in evidence, so fine chemicals companies need to get involved in printed electronics at an early stage. They cannot just jump in at the last minute because they are expert in certain elements and compounds. They cannot assume that printed electronics is largely a distant dream. For example, with over 360 organisations developing printed transistors, it would be unwise to presume that none of them will be selling any in 2009. Silicon chip materials are a bridge to printed electronics but you do need to cross that bridge.

For more attend Printed Electronics USA 2008.