This report investigates the market for various die and substrate attach materials used in power electronics in various electric vehicles. It builds a detailed quantitative model to forecast the addressable market size for die as well as substrate attach materials in various power electronic functions in all manners of electric vehicles. It also develops ten-year market forecasts, in value and mass, segmenting the market by material type. The materials considered herein include nano silver sintering, micro-silver sintering, Cu sintering, SAC and other solders, and transient liquid phase bonding materials.

The report provides a comprehensive view of the industry trends, looking at the trends driving the adoption of higher performance die attach materials; assessing how the packaging solutions including the die attach, the interconnect, and the cooling mechanisms are evolving to meet the more stringent needs of the industry; and examining the various existing and past implementations of power modules in leading electric vehicles on the market. The report also provides a comprehensive review of all firms offering metal sintering solutions around the world.

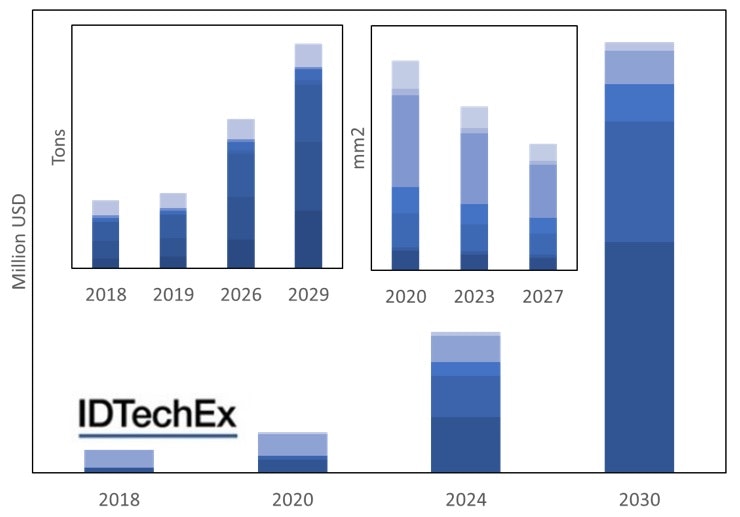

Main chart: market forecast for various die attach materials used both as die and substrate attach. The materials here include, in no particular order, SAC and other solders, Cu sintering, TLB, and micron and nano Ag sintering. The change in the mix of material will impact the market value due to price differentials. The left inset: forecast of addressable market only for die attach in tones segmented by electric vehicle category, e.g., mild hybrid, plug-in hybrid, forklift, bus, motorbike, etc. Right inset: forecast of aggregate die area segmented by power electronic function, e.g., charger, DC/DC, inverter, and so on. For more information and exact numbers please consult the report or contact us.

Background

The electric vehicle market is expanding. As a consequence, the market for power modules within all manner of electric vehicles is expanding. This, in turn, will translate into rising demand for materials, including die attach materials, used in power electronic packages and modules.

Our team has been researching the electric vehicle market for the past 15 years. Uniquely, this ongoing in-house research examines a diverse range of electric vehicles including 48V hybrid, plug-in hybrid, hybrid, full electric vehicles as well as electric forklifts, buses, motorbikes, scooters, drones, and so on. Many of these numbers underpin our forecast models.

The power electronic technology itself is also changing. In this report, we first provide an overview and benchmarking of various semiconductor technologies (Si, SiC, GaN). Here, we consider the benefits of each material technology at the material and device level. We then outline their key target applications in terms of voltage and power requirements. We will highlight some of challenges facing wide-bandgap semiconductors. More specifically, we will argue that these new technologies are not a drop-in replacement for Si MOSFET or Si IGBT. Many package designs and driving schemes and circuits will have to adapted to enable the optimal use of these technologies. We will then consider the commercial rational for deploying SiC in high-range full-electric vehicle inverters even though SiC is, and is likely to remain, more expensive than Si even if, as is well underway, its production shifts to larger wafer sizes.

Of particular interest to this study is the trend of rising areal power densities, which translates into higher operational temperatures. Indeed, the temperature is already pushed to 170C from 70C or so around early 2000s, and the industry wishes to push it further towards 250C.

This trend is partly aided by the transition towards wide bandgap materials such as SiC and GaN which can tolerate high operating temperatures. These materials will push the temperature bottleneck away from the device junction temperature to packaging materials. These materials will also enable smaller dies to handle large power levels, thus increasing the areal power densities. The combination of the trends towards high power density levels and more efficient higher frequency operation (which shrinks passive component size) will result in smaller and more integrated power electronic packages. To accommodate this and other trends, the packaging technology will have to adapt and is adapting. Indeed, this trend will push many materials including most solders beyond their performance limits, thus opening the door to alternatives.

In this report, we will first examine how the interconnect technology is moving away from the classical aluminium wire-bonding, which (a) suffers from low thermal conductivity, (b) does not lend itself to double-sided cooling, and (c) is a common point of failure. We will review many alternative approaches including (1) Cu wire bonding on Cu metallized die pads; (2) soldered/sintered Cu leads/clips/pins w/ or w/o spacers; (3) Cu wire bonding to sintered buffer plates; (4) metallized flexible film attachment with adhesives; and (5) Flex PCB attachment with metal sintering. Note that this topic relates to attachment materials because in some implementations, for example, a sintered metal or a solder is deployed.

In next section, we examine the limitations of solder technology as a die attach material. We consider the maximum operating temperature of various solder chemistries and show how the homologous temperature of solder technology, especially lead- and gold-free ones, are low, leading to high likelihood of failure as operating temperatures approach 175-200C. We then benchmark metal sintering vs various solder technologies, showing that metal sintering can offer bulk-like melting temperatures, high thermal conductivity, and a relatively low CTE mismatch with copper. We also compare the price levels of various options.

We then review how metal sintering has been used or demonstrated by various companies including ABB, ST Micro, Semikron, Infineon, StarPower, Danfoss, Continental, Siemens, Microsemi, CRRC, Fuji Electronic, and Hitachi. Indeed, it is clear that most makers today have the ability to work with metal sintering technology.

We then provide an overview of inverter power modules used in various hybrid and full electric vehicles. The power module deployed by various vehicle manufacturer is, directly or by extension, examined. These overviews will include inverters used by General Motors, Hyundai, Volkswagen, Daimler, Nissan, Honda, BMW, Tesla, and so on. The module maker is also highlighted. This section highlights the various design and material choices made by each player in terms of substrate, cooling technology and design, die and substrate attach, and so on. Trends will become clear despite the fact that multiple designs exist and are proven to work with the current requirements. As stated before, these designs will evolve to keep in line with future requirements and emerging semiconductor technologies.

We will then cover the materials, process, and suppliers of metal sintering die attach pastes. We first discuss the key characteristics of pressured metal sinter pastes looking at sintering process conditions, the shear strength of the joints, and the relationship between sinter pressure and porosity of the sintered layer. We also highlight some equipment used in pressured sintering. We will further discuss how product form factor is evolving beyond just pastes towards pre-forms and dry transfer films to render metal sintering as much of a drop-in replacement as possible. Finally, we consider pressure-less sintering. here, we discuss typical challenges including the conventionally long sintering time and the difficulty of sintering large-area dies without forming too many drying channels.

We then focus on suppliers of Ag and Cu sintering pastes. Here, we provide a comprehensive overview of companies including Heraeus, Alpha Assembly, Namics, Kyocera, Bando Chemical, NBE Tech, Mitsubishi Materials, Indium, Henkel, Nihon Superior, Dowa, Nihon Handa, AmoGreen, Mitsui Mining, Hitachi Chemical, and others.

We then build a detailed forecast model. Our model first estimates the power levels and the die area used in each power module function in each vehicle type considered. Here, we consider chargers, inverters, DC/DC converters, and so on. Next, we develop die area forecasts as a function time. This is based on studies of multiple current implementations. In general, the die area is shrinking as dies become better able to handle higher power levels, enabling the use of smaller and fewer dies. Note that the rise of SiC technology will aid this process. This step will then allow us to build our addressable market forecasts for die attach materials in terms of material volume or mass. Next, we study various implementations to estimate the addressable volume market for the substrate-to-baseplate attachment. Here, we considered multiple factors including the larger areas, the thicker bondline, and the fact that not every power module implementation will require such an attachment. We then develop our market share projection by die attach technology for both die-to-substrate and substrate-to-baseplate uses. The die attach technologies considered include Ag nano sintering, Ag micron sintering, Cu sintering, SAC and other solder, and transient liquid phase bonding materials. Our model then develops material-specific ten-year forecasts in volume and in value. To find out more about the repot "Die Attach Materials for Power Electronics in Electric Vehicles 2020-2030" please visit www.IDTechEx.com/DAMats to find out more.