What are the biggest trends affecting the additive manufacturing materials market? There are numerous influential factors changing the 3D printing materials industry, which IDTechEx forecasts to increase at a CAGR of 18.6% over the next decade to reach US$29.5 billion in 2032. These factors include a growing need for higher performance materials, building a circular economy within 3D printing, changing methodologies for 3D printing materials development, and so many more. One of the most interesting points is how the dichotomy between "open" materials systems and "closed" materials systems (also known as platforms or architectures) affects the growth and utilization of materials for additive manufacturing.

3D Printing: Open vs Closed Materials Architecture. Source: IDTechEx - "3D Printing Materials Market 2022-2032"

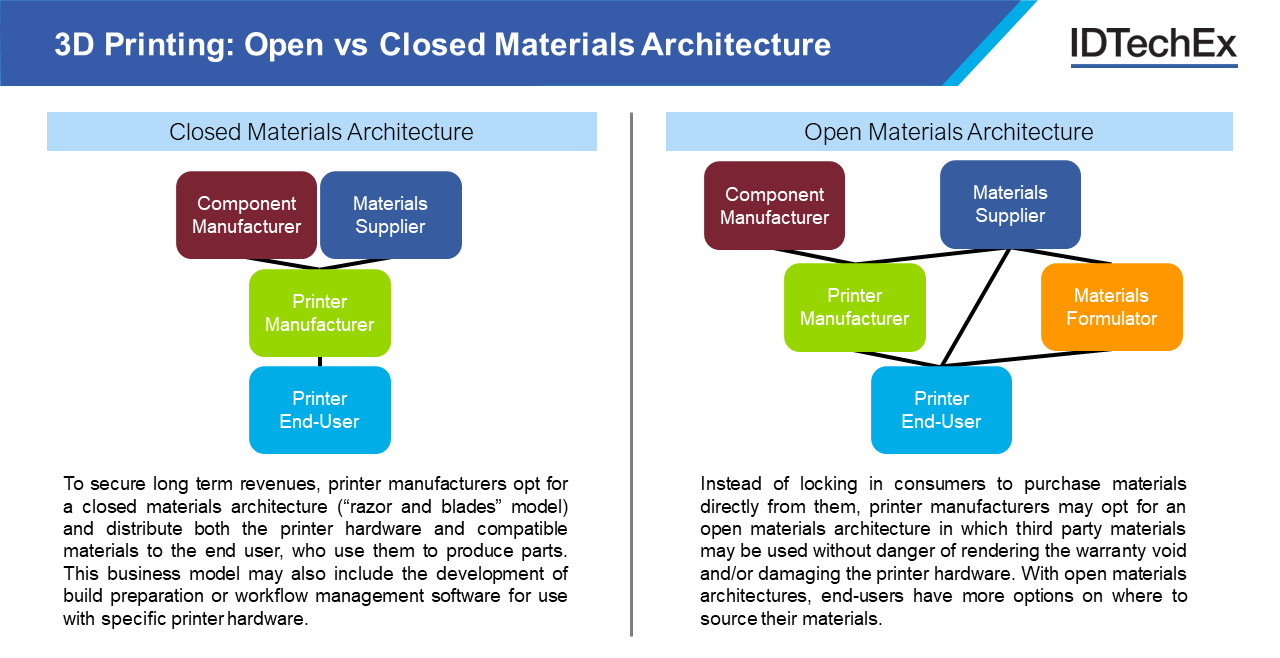

What are closed and open materials systems?

The concept of open and closed materials systems stems from the initial comparison between open-source 3D printers and closed-source 3D printers. Closed-source 3D printers utilize hardware, software, and materials made by the same printer manufacturer. With a closed materials system, end-users of the 3D printer can only use materials formulated and/or supplied by the printer manufacturer. This closed system was commonly used by legacy printer manufacturers like Stratasys and 3D Systems when additive manufacturing was in its early stages of development, as it simplified the adoption of 3D printing by its end-users by simplifying material selection and acquisition. Most importantly, closed materials systems help printer manufacturers secure long-term revenues by building a printer install base reliant on long-term consumables (I.e. 3D printing materials) purchases (similar to a "razor and blades" or "printer and ink" model).

As key 3D printing patents expired in the late 2000s and early 2010s, the competitive barriers to entry for printer manufacturers were blown away, leading to the rise of open-source 3D printers. Such printers, like those pioneered by the RepRap project, used widely available hardware components, open-source software, and most importantly, 3D printing feedstock from sources other than the printer manufacturer. With open materials platforms, printer end-users could utilize third party materials without the danger of rendering their printer warranty void, and/or damaging the printer hardware. The growth of this printer install base, which was not locked into a single supplier of materials, led to the establishment of many specialty 3D printing materials companies across polymer and metal 3D printing. With open materials systems, end-users now have multiple options for additive manufacturing materials suppliers:

- Printer manufacturers (like Creality and Prusa Research, who will often sell their own line of AM materials)

- Material suppliers (as raw material providers like Covestro, Evonik, and BASF now develop their own 3D printing materials to sell to printer manufacturers and end-users);

- Materials formulators (like Uniformity Labs and Liqcreate, who focus only on developing 3D printing materials)

- The end-user themselves (who may be researching or developing their own AM materials)

With open materials systems, a significant amount of flexibility is now placed in the hands of end-users with regards to the materials portfolio available to them. For hobbyists, open materials systems allow them to shop for cheaper materials from other manufacturers. For R&D scientists and academics, such systems facilitate cutting-edge materials development. From the perspective of materials suppliers and formulators, open materials systems exponentially increase the printer install base they can serve, as they would otherwise only have one channel to reach customers - the printer manufacturers.

What is the future of open and closed materials systems in 3D printing?

Across different levels of 3D printers (I.e. hobbyist, professional, and industrial), there has been a shift towards open materials systems for printers. This is particularly true in the polymer 3D printing realm, which historically utilized the closed materials system. For printer manufacturers, especially recently established ones, the open materials system allows them to focus limited resources on hardware development. Meanwhile, materials suppliers see the shift towards open materials systems as essential to growing the materials market for 3D printing, as they enable economies of scale to produce 3D printing materials at lower costs. This point is relevant for end-users, as a common barrier to entry for additive manufacturing is the high cost of materials.

However, many printer manufacturers remain reluctant to shift to a completely open materials ecosystem for their printers. First, revenue from consumables is important in the long-term, as 3D printers begin to saturate their target audiences; for this reason, it is difficult for printer manufacturers to undercut such an important long-term revenue stream. Second, as additive manufacturing technologies mature into more demanding and higher volume production applications, reliability and consistency "out of the box" are becoming much more important for end-users. Part of guaranteeing print reliability is establishing that a certain material will print well on a certain printer using optimized processing parameters. Realistically, printer manufacturers cannot validate and optimize the processing parameters for every third-party material on their printers; however, they can do that for a certain set of materials, like their own first-party feedstock. Therefore, closed materials systems allow for printer manufacturers to guarantee certain material performance without end-users needing to optimize print conditions themselves. In fact, the need for print reliability prompted Formlabs to close their latest generation of stereolithography (SLA) printers, after previous generations had open materials architecture. Others, like Meltio, are developing their own material feedstock validated and optimized for their open materials printers to address "out of the box" print reliability.

To try and balance between open and closed materials systems, many companies are opting into hybrid materials systems; in such systems, printer manufacturers do provide their own validated and optimized materials, but they also validate other companies' materials on their own platform. In 2021, Stratasys, a historic manufacturer of closed materials printers, shifted into a similar hybrid materials system called the Open Materials License.

Hybrid systems attempt to combine the flexibility of open materials systems with the reliability (and revenue opportunity) of closed materials systems. Importantly, they represent the balancing act that the industry is trying to manage, where on one hand, the additive manufacturing industry moves to expand its materials portfolio to reach new applications, while on the other hand, it looks to make 3D printing more reliable for production-level needs. IDTechEx expects the transformation of materials platforms in 3D printing to continue influencing not only the materials portfolio available but also how these materials reach end-users over the coming decade.

Market forecasts for Additive Manufacturing Materials

The 3D printing materials market report from IDTechEx forecasts future revenue and mass demand for the AM materials market while carefully segmenting the market by seventy-five different forecast lines across four major material categories. Additionally, IDTechEx provides comprehensive material benchmarking studies alongside detailed analysis on the AM materials market. For further information on this market including interview-based profiles of market leaders and start-ups, polymer material comparison studies, and granular 10-year market forecasts, see the market report "3D Printing Materials Market 2022-2032".

For more information on this report, please visit www.IDTechEx.com/3DPMats, or for the full portfolio of 3D Printing research available from IDTechEx please visit www.IDTechEx.com/Research/3D.

IDTechEx guides your strategic business decisions through its Research, Subscription and Consultancy products, helping you profit from emerging technologies. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.