IDTechEx's report Organic Photovoltaics 2013-2023: Technologies, Markets, Players analyses the latest developments in this field. This report gives an overview of the greater photovoltaic business landscape, assesses the organic photovoltaic technology at material and component level, and delivers detailed market forecasts.

The report also examines crucial components such transparent conductive films and barriers, outlining the needs, the latest developments and key players. These are crucial components whose value chain is adjacent to that of OPVs. The report builds technology roadmaps and detailed cost breakdowns by component.

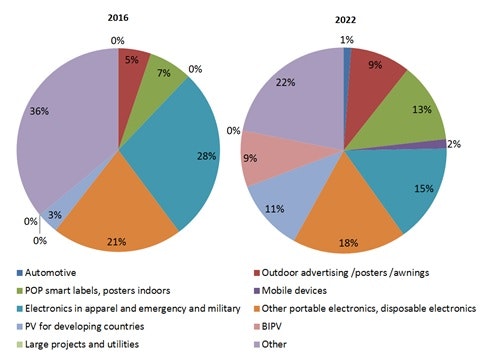

The ten-year forecasts focus also on niche applications (beyond utility) where OPVs may deliver value based on their key positive attributes. The sectors considered are street furniture, apparel, customer electronics, off-grid applications, posters and BIPV amongst others. The pie charts below depict the contribution of each market sector to the overall OPV market in 2016 and 2022.

IDTechEx has been tracking both organic and printed electronics markets and technologies for a number of years. It has maintained an up-to-date report on organic photovoltaic technologies, has carried out many consultancy projects, and has organised three conferences per year on the topic in three continents for the past six years, enabling it to know all the key players in the value chain of organic photovoltaics. At the same time, IDTechEx regularly visits and/or interviews key players in order to make detailed company profiles.

Figure 1: Pie chart showing the market split between different sectors by value in 2016 and 2022

Source: IDTechEx

Different markets will develop at different rates and some will never take off.

Photovoltaic industry is on the cusp of recovery

The photovoltaic industry is emerging from a period of rapid and intense consolidation. The industry experienced several years of oversupply as production capacity rapidly increased, spearheaded by Chinese companies making crystalline silicon cells, and demand was reduced thanks to government subsidises being slashed. The prices dramatically declined, changing the business landscape so rapidly that companies did not have the time to adapt. This triggered a wave of bankruptcies, mergers, acquisitions and closures. The price reduction also strengthened the position of wafer-based silicon photovoltaics as the dominant force. All the while however, the installed capacity during this period continued to expand while demand outside Europe also registered strong growth. The industry is recovering.

A game of niche markets

Organic photovoltaics are an emerging technology into this business landscape. Today they underperform when performance is only measured in efficiency and are over-priced when cost is measured in $/W. The industry has also experienced recent high-profile setbacks with Konarka, a highly visible company in the field, going bankrupt. This may however slowly change.

Manufacturers are working to identify niche market sectors that exploit the strengths of organic photovoltaics. These markets may value robustness (e.g., reduced vandalism), rollability (e.g., ease and speed of transfer and installation), low weight, colour control, and most importantly, ability to work under cloudy, low-light and indoor lighting conditions. At the same time, the material supply base remains strong while large printing/manufacturing companies with scale are also showing commitments to the technology, which will further alter the manufacturing business landscape that is today dominated by small firms. he OPV business will remain a niche play in the medium term. Companies will therefore have to be creative and work closely with end users to develop custom niche products. Therein lies the challenge.

Cost reduction trends

Two major cost drivers in an OPV stack are the barrier (encapsulation) and transparent conductive film layers. Rigid glass is an excellent encapsulation layer but it robs OPVs of a key selling point, which is mechanical flexibility. High-performance flexible multi-layer barrier films are notoriously challenging and expensive to manufacture. The picture may however change in the medium term given that many large companies have advanced programmes and strong pressure is building up in the value chain. This activity is being pulled by unmet needs from the OLED lighting and OLED display industries. Ultra-thin flexible glass is also in the race. A significant cost reduction in flexible barriers will help alter the economics of OPVs.

Transparent conductive films are another major cost driver in an OPV stack. OPVs require large-area, flexible and low sheet resistance transparent conductive layers. Low sheet resistance is vital because it affects efficiency while flexibility is important as it enables OPVs to differentiate from several other PVs technologies on the market. ITO dominates this business but it has limitations in terms of sheet resistance and flexibility (it can flex a little but not too much or too many times). Many alternatives are emerging including silver nanowires, metal mesh, carbon nanotubes, graphene, PEDOT, etc. Silver nanowires and metal mesh are ahead of the rest commercially. Performance improves and cost reductions on this front will also help improve the economies of OPV systems.

DSSC (dye sensitised solar cells) are a similar technology to OPV. They occupy the same market space and offer similar characteristics whilst also suffering from similar challenges and drawbacks. DSSC companies have also been under severe pressure lately with several notable firms having become bankrupt. Perovksite sensitised materials are a promising alternative that has emerged out of the blue, registering rapid performance improvement over a short period (a steep learning curve). This technology already shows much higher efficiency levels, at lab levels, than those reported for OPV and DSSCs. It can therefore be a further pending threat.

Conclusion

In summary, great uncertainly remains over the future of the OPV market as a whole, and arguably the industry is going through the period of despair and disillusion. The supply chain on polymer or organic material supply remains dominated by many large corporations that can quickly scale up should the demand rise. The scientific knowledgebase is strong and material formulations are multiplying every year. The performance of transparent conductive films and multi-film barriers is also improving while the price is falling This is thanks to synergies with other sectors with large tantalising addressable markets such as OLED displays and touch screen markets. These are all welcome trends that will have favourable long-term impacts. In the medium term, it will remain a niche play therefore companies will have to develop more realistic long-term product roadmaps, consisting of many niches, that seek to capitalise on the unique attributes of OPVs. .

Contact us

UK: +44 (0)1223 812300

US: +1 617 577 7890